December 07, 2020

Rapid Shift to Digital Banking During COVID-19 Accelerating Erosion in Consumer Trust, Accenture Report Finds

Banks must earn consumer trust if they hope to provide lucrative advisory services as a cornerstone of their growth strategies

NEW YORK, LONDON and HONG KONG; Dec. 7, 2020 – The replacement of in-person branch interactions with impersonal digital transactions through online and mobile channels during the COVID-19 pandemic has accelerated the ongoing erosion of consumer trust in banks, according to a new report from Accenture (NYSE: ACN).

Accenture’s 2020 Global Banking Consumer Study, based on a survey of more than 47,000 consumers globally, builds on two similar reports from 2019 and 2017. The latest report reveals that without a strong emotional connection with their bank, customers are more likely to view banking services as a commodity, with price being the ultimate competitive differentiator. Specifically, nearly four in 10 consumers (37%) ranked value for money as a top three factor, making it the most important factor when dealing with a bank, an increase of 10 percentage points from two years ago.

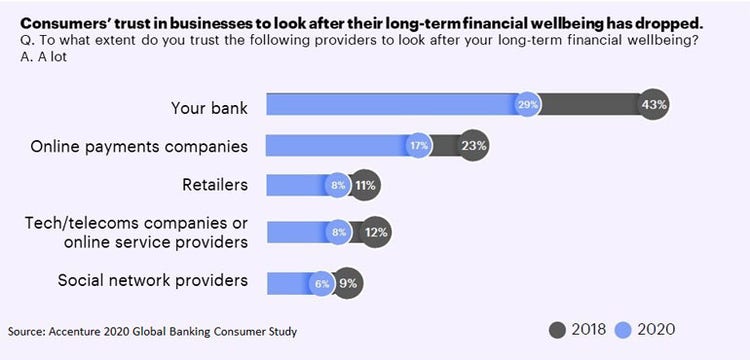

The report notes that while banks have long been encouraging consumers to use digital channels for transactional banking activity, there was no way to predict how aggressively that trend would accelerate as a result of COVID-19. While banks often view broader digital adoption as a way to lower costs and provide services 24/7, the rapid pivot to existing and hastily launched digital services has all but removed the vital human element from banking, further eroding consumer trust. For instance, less than one-third (29%) of surveyed consumers trust banks “a lot” to look after their long-term financial well-being, compared with 43% two years ago.

"At a time when customer trust is critically important, the recent shift to digital is threatening the relationships banks have worked to develop,” said Alan McIntyre, who leads Accenture’s Banking industry group globally. “The pandemic-inspired increase in digital engagement is a double-edged sword for banks. While it has allowed them to serve customers efficiently throughout the pandemic—and advanced their digital strategies by up to five years in some cases—it has pushed them to launch solutions that are functionally adequate but devoid of emotion. To forge strong customer connections, banks must reimagine the digital services they provide and make those connections more personal and relevant.”

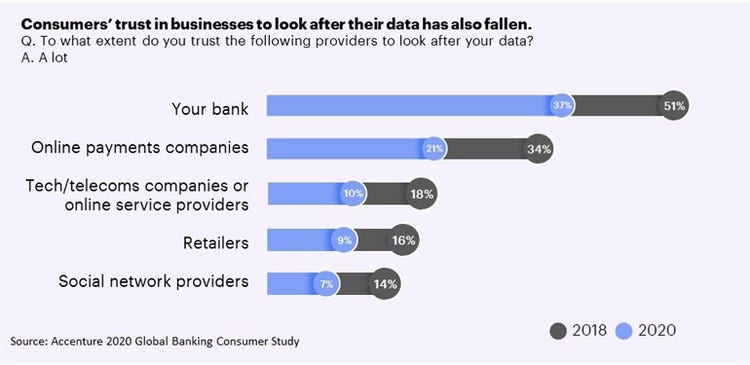

When asked how much they trust their bank to look after their data, fewer than four in 10 (37%) said “a lot,” a 14 percentage-point drop from just two years ago. Yet while overall trust might be eroding, the report found that more than half (57%) of consumers believe that when providing advice, their bank has their best interest in mind “always” or “most of the time,” and 62% believe that the advice is smart, personalized and well-informed.

These factors likely contribute to why nearly one-quarter (23%) of consumers believe that banks are in the best position to provide them with products and services outside of their core areas of expertise, compared with only 16%, 12%, and 11% of respondents who said the same for tech providers, social media companies and neobanks, respectively.

Permanent behavioral shift or pandemic-inspired fad?

The report suggests that banks need to evaluate how consumer behavior has been affected by the pandemic and determine which behavior changes are permanent – noting, for instance, the growing popularity of video calls. Prior to COVID-19, only 15% of consumers had spoken to a bank advisor via video call, but nearly half (46%) said they would be willing to do so when branches reopen, and 35% said they would prefer video calls to face-to-face meetings.

However, banks need to understand how different channels affect consumer trust. For instance, when receiving advice on products and offerings, only 28% of consumers said they would trust a human advisor “a lot” delivering advice over a video call, compared with 36% and 48% who said they would trust a human advisor “a lot” delivering advice by phone or in person in a branch, respectively.

“Banks must embrace how evolving consumer behaviors are driving change and create digital tools that add relevance and personality into each interaction with the ability to swap in a human advisor at the right moment,” McIntyre said. “The right approach will balance human and machine interactions, blending the convenience of more personalized digital interactions with human assistance when needed to create more value. This would go a long way toward reinforcing banks’ relationships with their customers, which in turn can build trust, loyalty and benefits for both.”

Evolution of switching

The report found that bank-switching behaviors, once a real-time indicator of increased competition or unhappy customers, have changed over the past two years. Primary account switching activity has decreased significantly, with just 3.8% of consumers saying they switched their primary bank account in the past 12 months, compared with 6.7% two years ago.

Noting that these low numbers can be attributed to the natural slump in neobank adoption after the initial surge, coupled with incumbent banks improving their digital capabilities, the report suggests that they could also provide a false sense of security for incumbents. Measuring switching has become more complex as consumers supplement their primary bank account with additional accounts that serve specific purposes — resulting in multi-banked customers.

“Switching has gone from a hard ‘cutting of the cord’ to a more dangerous slow-drip erosion of share of wallet,” McIntyre said. “This shows that the consumer/bank relationship is becoming even more fragmented, as consumers can quickly and easily open and place their money across various accounts to achieve specific financial goals or simply hedge their bets. The acceleration to digital has helped many traditional banks close the technology innovation gap with neobanks. Better digital offerings combined with the trusted stability of established banks may see the scales tipping to traditional banks as the preferred primary account for consumers.”

The full report can be accessed here: www.accenture.com/us-en/insights/banking/consumer-study-making-digital-banking-more-human.

Methodology

Accenture surveyed 47,810 respondents across 27 countries: Australia, Belgium, Brazil, Canada, China (including Hong Kong), Denmark, Finland, France, Germany, Ireland, Israel, Italy, Japan, Malaysia, Mexico, the Netherlands, Norway, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, United Arab Emirates, the United Kingdom and the United States. Respondents were required to have a bank account and covered multiple generations and income levels. The survey was conducted online during July and August 2020.

About Accenture

Accenture is a global professional services company with leading capabilities in digital, cloud and security. Combining unmatched experience and specialized skills across more than 40 industries, we offer Strategy and Consulting, Interactive, Technology and Operations services — all powered by the world’s largest network of Advanced Technology and Intelligent Operations centers. Our 506,000 people deliver on the promise of technology and human ingenuity every day, serving clients in more than 120 countries. We embrace the power of change to create value and shared success for our clients, people, shareholders, partners and communities. Visit us at www.accenture.com.

Accenture’s Banking industry group helps retail and commercial banks and payments providers boost innovation; address business, technology and regulatory challenges; and improve operational performance to build trust and engagement with customers and grow more profitably and securely. To learn more, visit https://www.accenture.com/us-en/industries/banking-index.

Copyright © 2020 Accenture. All rights reserved. Accenture and its logo are registered trademarks of Accenture.

# # #

Contact:

Melissa Volin

Accenture

+1 267 216 1815

[email protected]