May 04, 2017

Distributed Generation an Ongoing Threat to Utility Revenues and Hosting Capacity, Accenture Research Shows

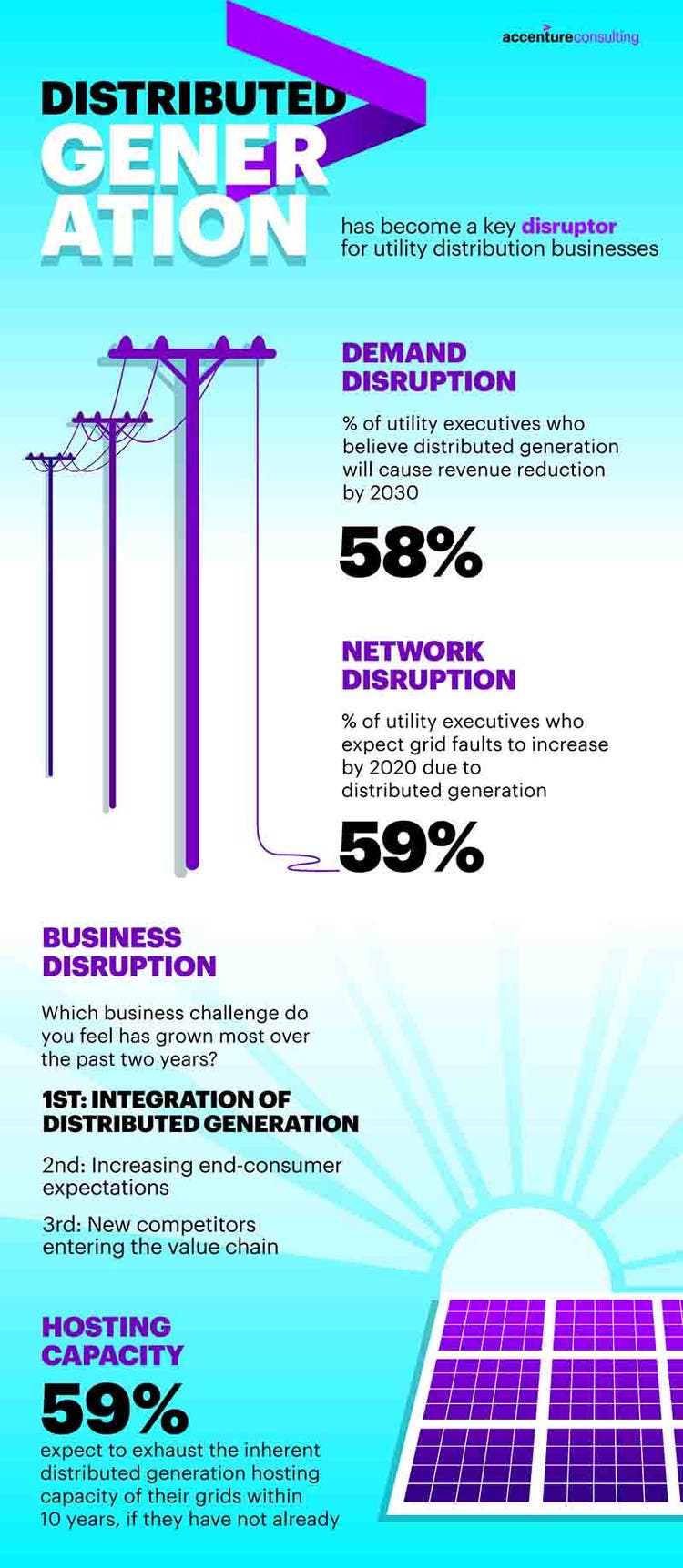

NEW YORK, May 4, 2017 – Utilities face the greatest risk of lost revenues from distributed generation (DG), including residential solar photovoltaics and fuel cells, according to Accenture’s (NYSE: ACN) Digitally Enabled Grid research, now in its fourth year.

The survey of more than 100 utilities executives across more than 20 countries revealed that 58 percent of distribution utility executives believe DG will cause revenue reduction by 2030. The concern is higher in North America and Asia Pacific than in Europe, due to the prevalence in these regions of vertically integrated utilities, which face the double impact of declining energy sales revenue and increased network costs to support reliable energy delivery.

Executives said the biggest DG-related stress on utilities’ network hosting capacity will come from energy prosumers who are driving small-scale DG (cited by 59 percent), followed by medium or high-voltage connected DG such as a large-scale solar plant (28 percent).

Accordingly, nearly six out of 10 executives (59 percent) expect grid faults to increase by 2020, due to more volatile uses of their networks triggered by the deployment of distributed renewable generation. In fact, 59 percent believe they will exhaust their DG hosting capacity within 10 years, if they haven’t already. After that, accommodating new DG on the distribution network will require increasingly high capital reinforcement costs. In the face of such disruption, only 14 percent of distribution utilities have a very clear forecast of their potential distributed generation network hosting capacity.

“The rapid evolution of the technology, better economics and the growing accessibility and environmental appeal of residential solar photovoltaics – or PVs – have pushed distributed generation from the fringe to a mainstream factor on the grid,” said Stephanie Jamison, managing director, Accenture Transmission and Distribution. “Combining solar PV with more economical options for battery storage, demand response, and energy efficiency will give consumers more power and require distribution utilities to provide more flexibility and different types of services. Despite the challenges the integration of these new technologies at scale bring, it is essential to meet the growing expectations of consumers in order to position utilities to provide services-based business models that could drive much-needed new revenue.”

Smarter Distributed Generation Integration Can Meet the Challenge

Utility executives identified the integration of distributed generation as the business challenge that has grown the most over the last two years. In response to the disruptive network impact of DG, a majority of utilities anticipate deploying a broad set of new capabilities over the next 10 years in network capacity planning, storage support and distributed generation operations. But there is still a long way to go.

”A balanced, network-wide approach is required to successfully integrate DG and enable utilities to benefit from its proliferation,” added Jamison. “The key will be to strike the right balance between prudent capital investments, optimizing operations and maintenance spending, while managing regulatory constraints on deployment and investing in smart solutions. This investment offers the opportunity to reduce the anticipated capital spending on network reinforcement and operating costs, while maintaining the quality and reliability of the power supply.”

Complementing the survey, Accenture economic modelling revealed that deploying customer-facing smart grid solutions could reduce capital spending for small-scale DG network reinforcement by around 30 percent by 2030 in the United States and Europe, equating to reductions of $6 billion and €16 billion, respectively.

The reductions in cost would be enabled by technologies that optimize networks for greater efficiencies across a more dynamic operating range. For example, locational incentives could steer investment to parts of the network with higher reinforcement costs; curtailment of DG output could be made at critical times, and storage and demand response services could be deployed.

Indeed, smarter DG integration has the potential to be a foundational component of the smart grid for many distribution utilities, providing cost-effective solutions to one of their most urgent challenges, according to Jamison.

Methodology

Accenture’s annual Digitally Enabled Grid research evaluates the implications and opportunities of an increasingly digital grid. The 2017 research included interviews with more than 100 utility executives across more than 20 countries between October 2016 and January 2017. The executives interviewed were those involved in the decision-making process for smart grid-related matters, with 71 percent representing integrated utilities and 29 percent standalone. The countries represented included Australia, Belgium, Brazil, Canada, China, Germany, Italy, Japan, Malaysia, the Netherlands, Norway, Philippines, Portugal, Saudi Arabia, South Africa, Spain, Switzerland, Thailand, the United Arab Emirates, the United Kingdom and the United States. Accenture also performed modelling to assess the costs of integrating small-scale distributed generation into the network and the potential saving on reinforcement capital costs.

About Accenture

Accenture is a leading global professional services company, providing a broad range of services and solutions in strategy, consulting, digital, technology and operations. Combining unmatched experience and specialized skills across more than 40 industries and all business functions – underpinned by the world’s largest delivery network – Accenture works at the intersection of business and technology to help clients improve their performance and create sustainable value for their stakeholders. With more than 401,000 people serving clients in more than 120 countries, Accenture drives innovation to improve the way the world works and lives. Visit us at www.accenture.com.

# # #

Contacts:

Guy Cantwell

Accenture

+ 1 281 900 9089

[email protected]

Matt Corser

Accenture

+ 44 755 784 9009

[email protected]