February 05, 2019

Most Utilities Executives Agree Risk of Consumers Going Largely Off-Grid Will Increase Significantly in Next Two Years, According to Research from Accenture

Stagnant electricity demand growth in the short term expected to turn around beyond 2025, as transport and heating electrification accelerates

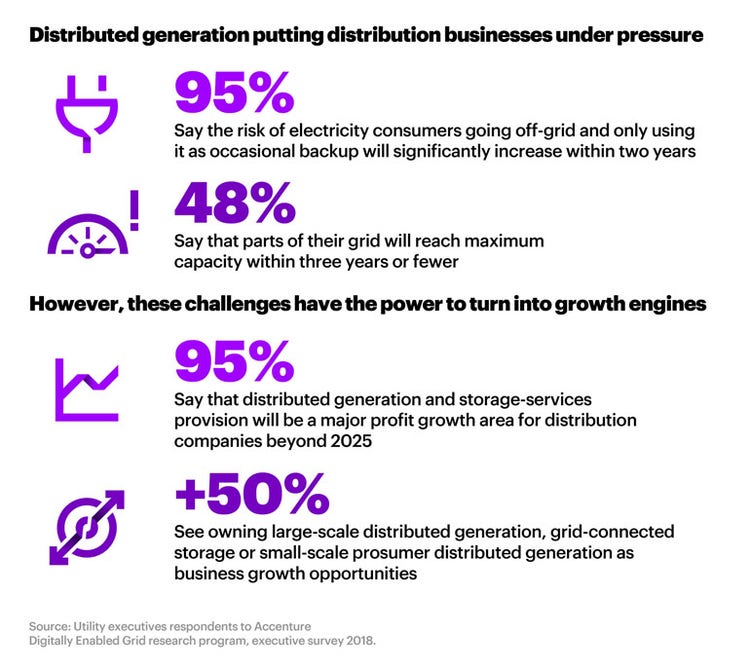

NEW YORK; Feb. 5, 2019 – Ninety-five percent of utilities executives agree that the risk of electricity consumers going largely off the grid and only using it as occasional backup will increase significantly in the next two years, according to a study from Accenture (NYSE: ACN), conducted as part of the company’s Digitally Enabled Grid research program.

The deployment of distributed generation (DG) technologies like rooftop solar is increasing faster than utilities can build new grid capacity to handle it in high-demand areas, according to the vast majority (95 percent) of the 150 executives surveyed across 25 countries. In fact, almost half (48 percent) of the respondents said that parts of their grid will reach maximum capacity in three years or less, with only 1 percent believing it will take longer than five years.

The proportion of both residential and commercial consumers with rooftop solar photovoltaics in the markets modelled could even exceed 15 percent by 2036 in some markets, such as California. This trend will likely continue to affect net electricity demand growth for the foreseeable future.

The study also notes that increased deployment of DG will complicate utilities’ operations, requiring distribution utilities to act now to avoid the excessive grid-reinforcement spending required to host new DG energy flows.

According to Accenture modeling, some markets could generate substantial capital reinforcement cost savings simply through better identification of local constraints on the distribution network. A 10 percent improved accuracy in DG forecasts, resulted in projected savings of 15-28 percent in New York, 14-18 percent in California, 14-15 percent in Australia, and 11-12 percent in both the United Kingdom and the Netherlands.

In fact, DG integration was ranked as the second-highest priority area as a cost-saving opportunity, selected by 59 percent of respondents as one of their top 5 choices. The top priority, chosen by 61 percent of respondents, was reducing supply chain unit costs through improved forecasting of materials and service requirements.

“Distribution businesses have had a tough time in recent years with weak demand, which is one reason why grid operators’ profits have been squeezed,” said Stephanie Jamison, a managing director at Accenture who leads its Transmission and Distribution business. “The proliferation of DG changes electricity demand profiles, potentially diminishing total demand without necessarily reducing peak demand. Successful DG integration will require substantial investments in new connections and grid reinforcement to modernize the network and sustain the same level of reliability and safety and secure operations.”

While DG presents a challenge to distribution utilities, it’s also an opportunity, with 95 percent of respondents saying that DG and storage-services provision will be a major profit growth area for distribution companies beyond 2025. More than half of respondents globally also identified owning each of the following assets as an opportunity for their business going forward: large-scale DG; grid-connected storage; small-scale prosumer DG; and community storage.

Electrification of transport and buildings will bolster electricity demand growth after 2026

Accenture modeling predicts that, following a period of stagnation, electricity demand could grow by 31 percent between 2026 and 2036. The study and modeling partly attribute the growth to the meaningful impact that electric vehicles (EVs) and building heating electrification will have on demand growth starting around 2025.

The modeling revealed that the total percentage of plug-in electric vehicles in the overall vehicle stock is forecast to grow relatively slowly, from 1 percent this year to 3 percent by 2025, but could rise to 37 percent by 2040, led by municipal buses, scooters and small commercial vehicles.

This trend could translate to substantial new electricity demand. Indeed, while the electricity consumption of EVs is expected to represent just over 1 percent of the annual peak demand hour by 2025, it is forecast to rise almost fourfold in the markets modelled by 2040, to 4 percent. In some markets like France and California, forecasts are even higher by that year (10 percent and 8 percent, respectively).

The decarbonization of buildings is also likely to push up electricity demand in the long term, with 96 percent of utilities executives agreeing that decarbonization efforts will substantially reduce residential and commercial natural gas demand by 2040.

Just the combined effects of transport and heating electrification could push peak demand up significantly, with Accenture modeling suggesting that the average electricity consumption during the peak demand hour could rise by around 63 percent from 2016 in 2040.

“Mass adoption of electric vehicles and the electrification of building heating is poised to alter demand growth and load shape in the longer term,” Jamison said. “This suggests high growth potential for utility distributors, but it will also put pressure on grid stability. The key will be to navigate this disruption by making the grid more resilient through greater use of smart technologies and utilizing all sources of flexibility including on the demand side, adopting a more customer-centric approach.”

Research Methodology

Accenture’s annual Digitally Enabled Grid research evaluates the implications and opportunities of an increasingly digital grid. For the most-recent research, Accenture surveyed 150 utility C-suite and Senior Vice-President level executives from 25 countries: Argentina, Australia, Brazil, Canada, China (including Macau and Hong Kong), Denmark, France, Germany, Indonesia, Ireland, Italy, Japan, Malaysia, the Netherlands, Norway, the Philippines, Poland, Portugal, Singapore, Spain, Sweden, Switzerland, Thailand, the United Kingdom and the United States; the quantitative online survey was conducted in February and March 2018. In addition, Accenture developed a geographic-level electricity demand impact model to quantify the forecast combined hourly impact of individual electricity demand drivers for a selected sample of 18 countries (Australia, Belgium, Brazil, Canada, China, France, Germany, India, Italy, Japan, Mexico, South Korea, the Netherlands, Poland, Spain, Sweden, Switzerland and the United Kingdom) and five of the most-populous U.S. states (California, Texas, Florida, New York and Illinois).

About Accenture

Accenture is a leading global professional services company, providing a broad range of services and solutions in strategy, consulting, digital, technology and operations. Combining unmatched experience and specialized skills across more than 40 industries and all business functions ? underpinned by the world’s largest delivery network ? Accenture works at the intersection of business and technology to help clients improve their performance and create sustainable value for their stakeholders. With 469,000 people serving clients in more than 120 countries, Accenture drives innovation to improve the way the world works and lives. Visit us at www.accenture.com.

# # #

Contacts:

Guy Cantwell

Accenture

+1 281 900 9089

[email protected]

Matt Corser

Accenture

+44 755 784 9009

[email protected]